TARP stands for Taxpayer Assistance and Relief Program. It was a U.S. government program initiated in 2008 to help stabilize the financial markets during a severe economic crisis. While the specific program has concluded, understanding its purpose offers insight into financial protections.

It can be confusing when you hear acronyms like TARP, especially when they relate to financial matters or government initiatives. You might wonder what these letters actually mean and why they matter. Don’t worry, you’re definitely not alone! Many of us encounter these terms and feel a bit lost, wanting a clear, simple explanation that makes sense. This guide is here to break down exactly what TARP stands for and what it was all about, in a way that’s easy to grasp.

We’ll explore its origins, its purpose, and what happened to it. By the end of this article, you’ll have a solid understanding of TARP and how it relates to financial stability. Let’s get started!

What Does TARP Stand For? The Simple Answer

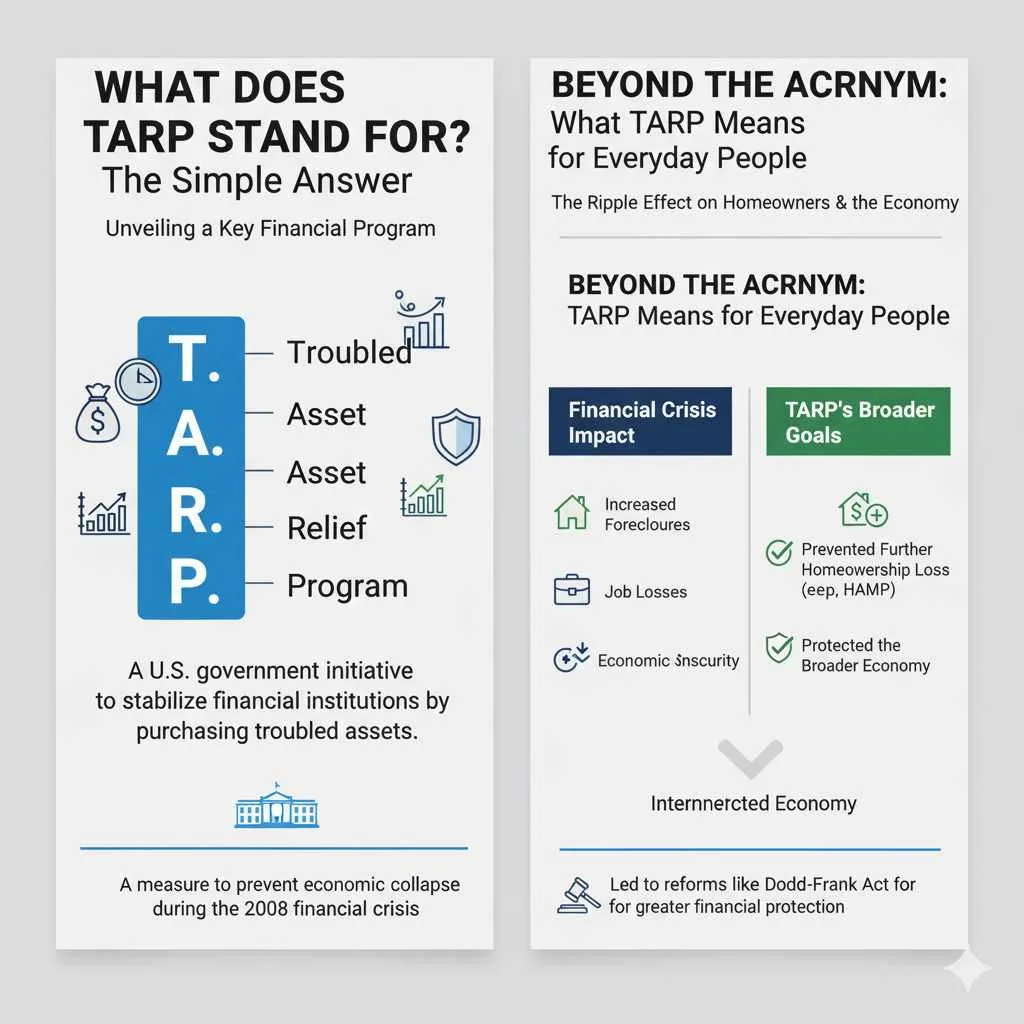

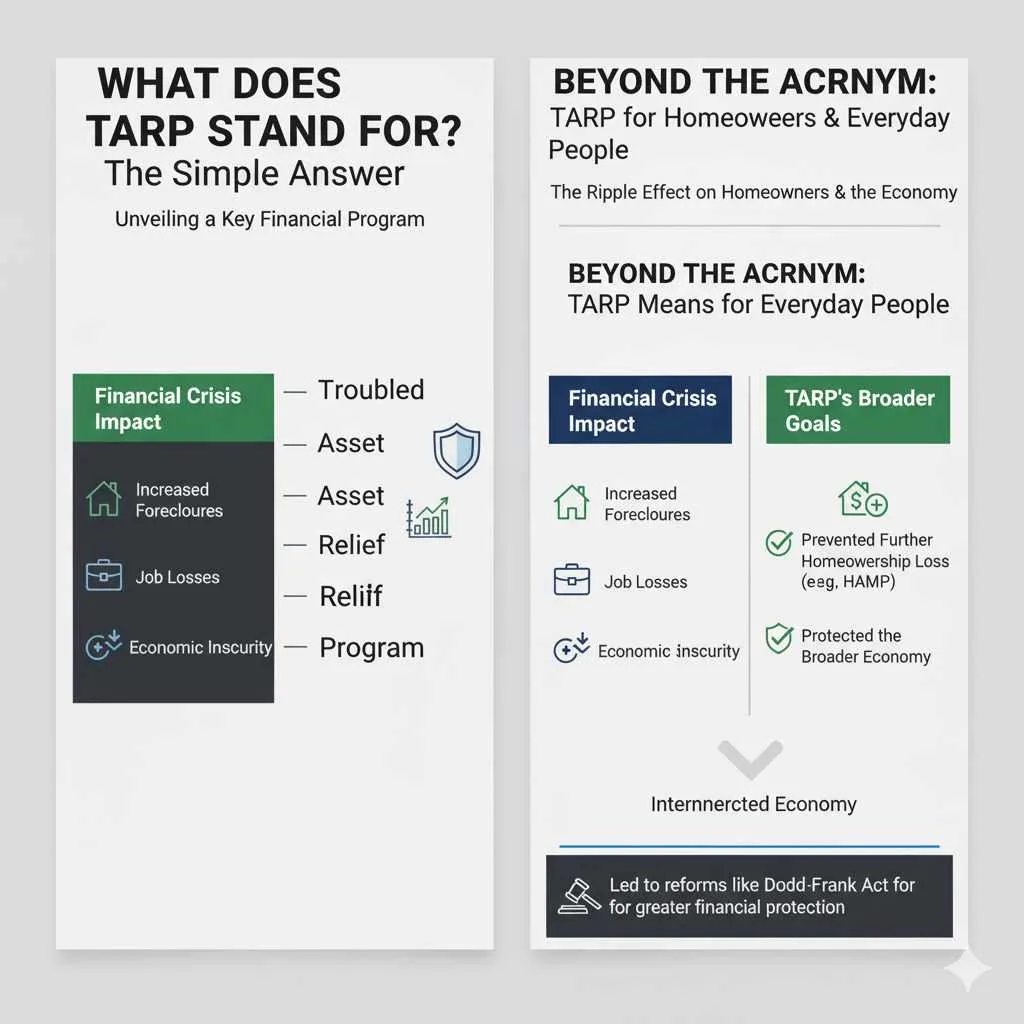

The acronym TARP officially stands for the Troubled Asset Relief Program. While it originated in the United States as a response to a financial crisis, the term itself is straightforward and describes its core function: providing relief by addressing troubled assets.

This program was a significant government intervention designed to prevent a complete collapse of the financial system. It allowed the U.S. Treasury to purchase or insure toxic assets from financial institutions, inject capital into them, and generally stabilize markets. Think of it as a helping hand for large financial companies when they were facing severe difficulties.

Unpacking TARP: A Deeper Dive

The Troubled Asset Relief Program (TARP) was signed into law by President George W. Bush on October 3, 2008. Its primary objective was to restore confidence in the U.S. financial system and avert a broader economic meltdown. The program authorized the Treasury to spend up to $700 billion, though not all of it was ultimately disbursed.

The economic landscape at the time was grim. The housing market had collapsed, leading to widespread defaults on mortgages. This, in turn, caused the financial instruments backed by these mortgages (like mortgage-backed securities) to lose their value dramatically. Banks and other financial institutions held vast quantities of these “toxic assets,” leading to massive losses, a freeze in credit markets, and a severe risk of widespread bank failures.

TARP was created as an emergency measure to inject liquidity into these failing institutions and remove the toxic assets from their balance sheets. The belief was that by cleaning up balance sheets and providing capital, banks would be more willing to lend money, thus preventing a domino effect of business failures and job losses.

Key Objectives of TARP

- Stabilize Financial Institutions: To prevent the collapse of major banks and financial firms, which could have had devastating consequences for the entire economy.

- Unfreeze Credit Markets: To encourage banks to lend to each other and to businesses and consumers again, which is essential for economic activity.

- Support the Housing Market: To help stabilize the housing market and prevent further foreclosures.

- Restore Investor Confidence: To signal to markets that the government was taking decisive action to address the crisis, thereby restoring confidence.

How Did TARP Work?

TARP employed several mechanisms to achieve its goals. The most prominent methods included:

1. Capital Purchases

The Treasury Department purchased preferred stock (a form of ownership) in various financial institutions. This injected much-needed capital directly into these companies, strengthening their financial positions. In return for this investment, the government received equity stakes, meaning it became a part-owner of these profitable enterprises. This was a crucial part of TARP, aimed at recapitalizing banks.

For example, the Treasury invested in major banks like JPMorgan Chase, Bank of America, and Citigroup. These investments provided these institutions with a financial cushion, allowing them to continue operating and lending.

2. Troubled Asset Purchases (TAPs)

Initially, TARP also envisioned the direct purchase of “troubled assets” – the devalued mortgage-backed securities and other complex financial products that were causing so much trouble. The idea was to buy these assets from institutions at a price that would help them avoid massive write-downs, thereby improving their balance sheets. However, this aspect of the program proved more complex and was later deemphasized in favor of direct capital injections.

3. Automotive Industry Financing

A significant portion of TARP funds was also allocated to assist the struggling U.S. auto industry, specifically General Motors and Chrysler. The loans provided were intended to prevent their collapse, which would have led to massive job losses and further economic disruption. This included loans to help restructure these companies and ensure their survival.

4. Home Affordable Modification Program (HAMP)

TARP also funded initiatives to help struggling homeowners avoid foreclosure. The Home Affordable Modification Program (HAMP), for example, was designed to modify mortgages to make monthly payments more affordable for homeowners. This was a direct effort to address the root cause of many financial institution’s problems – the housing crisis.

Who Received TARP Funds?

TARP funds were distributed to a wide range of financial institutions and corporations. The beneficiaries included:

- Major Banks: Including giants like Bank of America, Citigroup, JPMorgan Chase, and Wells Fargo.

- Investment Banks: Such as Goldman Sachs and Morgan Stanley.

- Insurance Companies: Most notably, the government provided a bailout to American International Group (AIG).

- Auto Manufacturers: General Motors and Chrysler.

- Mortgage Agencies: Fannie Mae and Freddie Mac.

The distribution of funds was a complex process, with different institutions receiving varying amounts and types of assistance. The goal was to address systemic risks, meaning the potential for the failure of one institution to trigger a cascade of failures throughout the financial system.

Here’s a simplified look at some key recipients and the scale of their involvement:

| Institution | Primary Type of Assistance | Approximate Amount Received (in billions USD) |

|---|---|---|

| AIG | Capital Injection (Preferred Stock) | $182.3 |

| Bank of America | Capital Injection (Preferred Stock) | $45.0 |

| Citigroup | Capital Injection (Preferred Stock) | $45.0 |

| General Motors | Loans and Capital Injection | $49.5 |

| Chrysler | Interim and Restructuring Financing | $12.5 |

| JPMorgan Chase | Capital Injection (Preferred Stock) | $25.0 |

Note: Amounts are approximate and represent a portion of the total TARP outlays for these entities. The total capital invested by the Treasury across all programs was eventually recouped, often with a profit. Data is consolidated from various sources, including the U.S. Department of the Treasury.

Was TARP Successful? The Results

Assessing the success of TARP is complex, with varied opinions. However, most analyses suggest that TARP achieved its primary objective: preventing a complete collapse of the financial system and averting a deeper depression.

Pros of TARP

- Prevented Systemic Collapse: TARP successfully stabilized major financial institutions, preventing widespread bankruptcies and a gridlock of credit markets.

- Restored Market Confidence: The government’s decisive action helped to calm panicked markets and begin the process of recovery.

- Financial Return to Taxpayers: Ultimately, the Treasury Department recouped more money than it invested through TARP. This was achieved as financial institutions repaid the capital injections, and the government sold its equity stakes, often at a profit. The U.S. Department of the Treasury reported a net profit on TARP investments.

- Economic Stabilization: By preventing a total financial meltdown, TARP is credited with mitigating the severity and duration of the recession.

Cons and Criticisms of TARP

- Moral Hazard: Critics argued that TARP created a “moral hazard,” where institutions took excessive risks knowing they might be bailed out by the government.

- Fairness: Some felt it was unfair for taxpayers to bail out large financial institutions that played a role in creating the crisis, while ordinary citizens faced job losses and foreclosures.

- Lack of Accountability: Questions were raised about the level of accountability for the executives whose decisions led to the crisis.

- Program Complexity: The program’s implementation was criticized for its complexity and the speed at which decisions were made.

Despite the criticisms, the consensus among many economists is that the intervention, although unpopular, was necessary to prevent a far worse economic outcome. You can find detailed reports and historical data on TARP’s outcomes from official sources like the U.S. Department of the Treasury’s website.

What Happened to TARP?

TARP was an emergency program, and its statutory authority expired in October 2010. However, the process of winding down the investments and ensuring repayment continued for several years afterward. The Treasury Department actively managed its stakes in companies and worked to recover the funds allocated.

By December 2014, the Treasury announced that all TARP investments had been repaid by the recipient institutions. More significantly, the program generated a profit for the government. This profit came from the repayment of loans and the sale of equity stakes in companies, proving that the government intervention ultimately resulted in a net gain for taxpayers.

The legacy of TARP is mixed. It’s remembered as a controversial but critical intervention that helped steer the U.S. economy away from a catastrophic depression. The lessons learned from TARP have influenced subsequent financial regulations, aiming to prevent similar crises from occurring or to manage them more effectively if they do.

Beyond the Acronym: What TARP Means for Homeowners and Everyday People

While TARP directly involved large financial institutions, its effects rippled through the economy, impacting everyone. For homeowners, the crisis that led to TARP meant increased foreclosures, job losses, and a general sense of economic insecurity. The parts of TARP that supported programs like HAMP were direct attempts to alleviate some of this pressure and prevent further homeownership losses.

Understanding TARP helps us see how interconnected our economy is. When large financial systems are in distress, the effects are felt far and wide. The program, though aimed at institutions, was ultimately a measure to protect the broader economy, including the livelihoods and homes of everyday Americans.

For those interested in the details of financial regulations born from this era, you might explore resources explaining the Dodd-Frank Wall Street Reform and Consumer Protection Act, which was enacted in 2010 partly in response to the lessons learned from the 2008 financial crisis and the interventions like TARP. Understanding these events can empower you to be more informed about economic policies and their real-world impact.

Frequently Asked Questions About TARP

Here are some common questions people have about the Troubled Asset Relief Program:

Q1: What was the main reason for creating TARP?

The main reason was to prevent a complete collapse of the U.S. financial system during the severe financial crisis of 2008. It aimed to restore confidence by injecting capital into struggling financial institutions and stabilizing markets.

Q2: Did taxpayers get their money back from TARP?

Yes, the U.S. Department of the Treasury reported that all TARP investments were repaid by the recipient institutions. In fact, the program generated a net profit for the government.

Q3: Was TARP a bailout for rich bankers?

While it directed funds to financial institutions, the program’s stated purpose was to stabilize the entire economy, which would prevent widespread job losses and further suffering for all Americans. The funds were not simply given away; they were often investments in exchange for ownership stakes or loans that were meant to be repaid.

Q4: Did TARP help homeowners directly?

Parts of TARP funded initiatives like the Home Affordable Modification Program (HAMP), which aimed to help homeowners modify their mortgages to avoid foreclosure. So, while not all TARP money went directly to homeowners, some was allocated to programs that supported them.

Q5: What happened to the toxic assets TARP was supposed to buy?

The program did involve purchasing troubled assets, effectively clearing them from the balance sheets of financial institutions. However, the emphasis shifted more towards direct capital injections as the primary method of stabilization.

Q6: When did TARP officially end?

TARP’s statutory authority expired on October 3, 2010. However, winding down the program and managing the remaining investments and repayments continued for several years beyond that date.

Q7: Is TARP still active today?

No, TARP is not active today. All funds have been repaid, and the program officially concluded its operations. However, the impact of the 2008 financial crisis and the interventions like TARP led to significant changes in financial regulation.

Conclusion

So, what does TARP stand for? It’s the Troubled Asset Relief Program, a critical and often debated government response to the 2008 financial crisis. Its goal was to stabilize the U.S. financial system by providing capital to key institutions and helping to unfreeze credit markets. While it was a controversial measure, it played a significant role in preventing an even deeper economic downturn.

For us, as homeowners and everyday people navigating our own finances and home projects, understanding these larger economic events can provide valuable context. It highlights the interconnectedness of our economy and the importance of stability. Knowing that the government took action to address systemic risks, and that these actions ultimately resulted in a net financial recovery for taxpayers, can offer a sense of reassurance.

TARP is a chapter in recent economic history that, while complex, is important to understand. By demystifying terms like TARP, we empower ourselves with knowledge, making the world of finance and economic policy a little less daunting. Thanks for joining me on this exploration!